Are you planning to buy a car and feeling overwhelmed by all the financial advice out there? You’re not alone.

Navigating the world of car buying can be tricky, especially when it comes to managing your budget. But what if there was a simple formula to guide you? Enter the 20/4-10 rule when buying a car. This straightforward rule helps you decide how much you should spend on a car, how long you should finance it, and how it fits into your monthly expenses.

Curious to know more? Stick around, because understanding this rule could save you money and stress, helping you drive away with confidence.

Understanding The 20/4-10 Rule

Buying a car involves many decisions. One key factor is the 20/4-10 rule. This rule helps manage your finances effectively. It ensures you’re not overspending on a car purchase. Understanding this rule can make your car-buying journey smoother.

What Does The 20 Stand For?

The ’20’ in the 20/4-10 rule refers to the down payment. You should aim to put down 20% of the car’s price. This reduces the loan amount. It also lowers your monthly payments. A larger down payment can even get you better loan terms.

The Importance Of The ‘4’

The ‘4’ represents the loan term. Try to keep your car loan to four years. A shorter loan term means less interest paid over time. It also prevents you from being upside down on the loan. Paying off your car faster can improve your financial health.

Understanding The ’10’

The ’10’ is about your monthly budget. Spend only 10% of your monthly income on car expenses. This includes the loan, insurance, and maintenance. Keeping to this budget helps avoid financial strain. It ensures that your car expenses don’t disrupt other financial goals.

Benefits Of Following The 20/4-10 Rule

Following this rule offers many benefits. It encourages responsible spending. You avoid overspending on a vehicle. It helps in maintaining a balanced budget. Adhering to the rule also improves your financial security.

Credit: www.youtube.com

Components Of The Rule

Understanding the 20/4-10 rule is crucial for smart car buying. This rule offers a simple guideline. It helps you manage your car expenses wisely. Knowing its components can save you money in the long run.

The 20% Down Payment

The first component is a 20% down payment. This is the upfront cash you pay. It reduces the loan amount and interest. A larger down payment means less financial stress later.

Four-year Loan Term

The second component is a four-year loan term. It limits the time you spend paying off your car. Shorter loans mean you pay less interest overall. It keeps your car expenses manageable.

10% Monthly Expenses Cap

The final component is a 10% cap on monthly expenses. Ensure your car costs don’t exceed 10% of your monthly income. This cap includes insurance, maintenance, and fuel. It helps maintain a balanced budget.

Benefits Of Following The Rule

The 20/4-10 rule helps make smart car-buying decisions. Put down 20% of the car’s price. Finance it for four years. Ensure monthly payments don’t exceed 10% of income. This approach promotes financial stability.

When you’re considering buying a car, the 20/4-10 rule is a game-changer. This rule suggests you make a 20% down payment, finance the car for no more than four years, and ensure that car payments don’t exceed 10% of your monthly income. But why follow this rule? Let’s dive into its benefits and see how it can transform your car-buying experience.

Financial Stability

Adhering to the 20/4-10 rule can lead to greater financial stability. Making a 20% down payment reduces the loan amount, which means you owe less from the start. Having less debt boosts your financial confidence and security. Imagine not feeling overwhelmed by monthly payments; instead, you’re in control. This stability can open doors to future financial goals, like saving for a vacation or investing.

Reduced Interest Payments

A shorter loan term means fewer interest payments over time. Financing a car for just four years significantly cuts down the interest you pay. Think about the savings over those four years—money that could be spent elsewhere. By reducing interest, you keep more cash in your pocket. Doesn’t that sound more appealing than handing it over to the bank?

Improved Budget Management

Keeping car payments under 10% of your monthly income ensures you don’t overstretch your budget. It’s all about smart management. With this approach, you maintain flexibility in your finances. You can easily handle unexpected expenses without stress. Isn’t it reassuring to know your budget isn’t solely dictated by your car payment? This rule helps you manage your money, not let it manage you. Would you rather have peace of mind or worry about making ends meet because of a car payment? The choice is yours, and following the 20/4-10 rule can make all the difference.

Credit: tejimandi.com

Challenges In Adhering To The Rule

Adhering to the 20/4-10 rule when buying a car can be tough. Many face challenges saving 20% for a down payment. Maintaining a four-year loan term while keeping monthly payments under 10% of income adds complexity. Budget constraints make it hard to stick to this financial guideline.

Buying a car can be an exciting yet daunting process, especially when trying to adhere to the 20/4-10 Rule. This rule suggests that you make a 20% down payment, finance the car for no more than four years, and keep monthly payments below 10% of your monthly income. While this guideline can help you maintain financial stability, it presents certain challenges that can be difficult to navigate. Let’s explore these challenges and how you might overcome them.

Affording The Down Payment

Saving enough for a 20% down payment can be tough, particularly if you’re juggling other financial responsibilities. Imagine having to set aside a significant chunk of your savings or sacrificing certain luxuries to meet this requirement. Have you ever wondered how to prioritize saving without feeling deprived? One strategy is to create a dedicated savings account specifically for your car down payment. Automate transfers to this account to make saving easier and more consistent.

Finding Suitable Financing

Securing the right financing can be a maze of interest rates, loan terms, and lender requirements. You might find yourself overwhelmed by the options or uncertain about which choice best suits your financial situation. It’s crucial to shop around and compare offers from different lenders to find the most favorable terms. Are you aware of the potential impact of your credit score on the interest rates offered to you? Improving your credit score before applying can open doors to better financing options.

Balancing Monthly Expenses

Keeping your monthly car payment below 10% of your income can feel like a tightrope walk, especially if your budget is already stretched thin. You might question how to fit this payment into your existing financial commitments without sacrificing your lifestyle. Consider reviewing your current expenses to identify areas where you can cut back. Could you save by reducing dining out or finding cheaper entertainment options? Balancing your budget may require some adjustments, but the peace of mind that comes from financial stability is worth the effort.

Alternatives To The 20/4-10 Rule

While the 20/4-10 Rule is a popular guideline for car buying, it doesn’t suit everyone. Some people need alternatives that better fit their financial situation. These options offer flexibility and different approaches to car purchasing.

Shorter Loan Terms

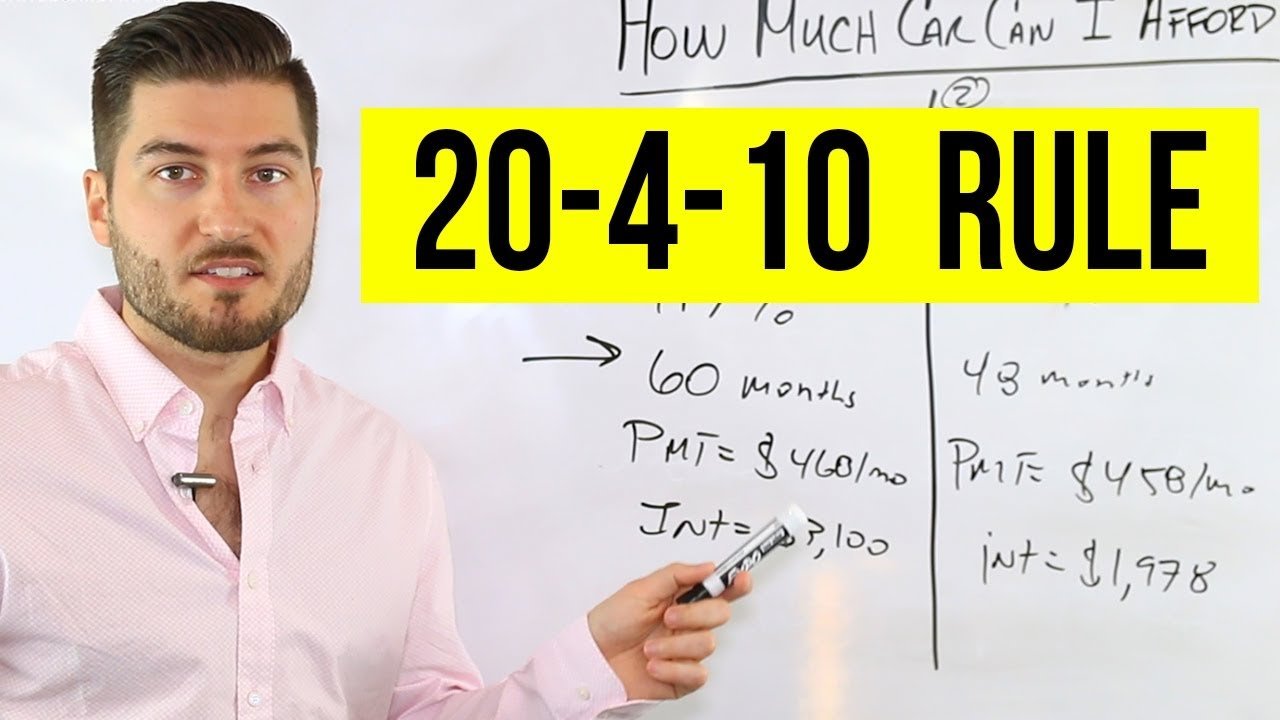

Consider a loan term shorter than 60 months. Shorter terms often mean less interest over time. Monthly payments might be higher, but you’ll pay off the car faster. This can save money in the long run. A shorter loan can also help you build equity faster.

Higher Down Payments

Another alternative is making a larger down payment. A higher down payment reduces the loan amount. This can lead to smaller monthly payments. It might also help secure a better interest rate. More upfront payment shows strong financial commitment.

Flexible Budgeting Strategies

Adopt flexible budgeting strategies to find the best car deal. Set a realistic budget that fits your needs. Allocate funds for insurance, maintenance, and other costs. Adjust your budget as needed to stay within financial limits. Use budgeting apps to track expenses and avoid overspending.

Credit: swaper.com

Tips For Effective Car Buying

Buying a car can be both exciting and daunting. You want to make sure you’re getting a good deal, but also a vehicle that suits your needs. The 20/4-10 rule is a handy guideline to keep your finances in check, suggesting you put down at least 20% of the car’s price, finance it for no more than 4 years, and ensure monthly payments don’t exceed 10% of your income. While this rule simplifies the financial aspect, effective car buying involves more than just numbers.

Researching Vehicle Options

Start by identifying your needs. Do you need a car for city commuting or long road trips? Each type has its pros and cons. For city driving, a compact car might be more efficient and easier to park. If road trips are your thing, consider a spacious SUV with excellent mileage.

Look into reviews and ratings online. Websites like Edmunds or Kelley Blue Book provide detailed insights into vehicle performance and reliability. You might stumble upon a hidden gem or a model with recurring issues to avoid.

Think about your lifestyle. A friend once bought a sleek convertible only to realize it wasn’t practical for his family of four. Lesson learned: visualize your daily routine with the car.

Negotiating With Dealers

Walking into a dealership can be intimidating, but remember, you hold the power. Start by understanding the market price. Knowing the average selling price for your desired model gives you leverage.

Don’t be afraid to ask for discounts or incentives. Dealers often have promotions or can lower the price to meet sales targets. A friend managed to snag a free maintenance package just by asking.

Be prepared to walk away. If the deal doesn’t feel right, trust your gut. Dealers might offer a better price once they see you’re serious about leaving.

Evaluating Long-term Costs

Consider the total cost of ownership, not just the sticker price. Fuel efficiency, maintenance, insurance, and depreciation all add up over time. A hybrid might save you on fuel, but check if its parts are more expensive.

Think about the car’s resale value. Some brands hold their value better than others, which can save you money when it’s time to sell or trade in. My cousin once bought a car that depreciated rapidly, leaving him in a financial pinch.

Ask yourself, is this car the best financial decision for the future? Will monthly payments strain your budget, or will it still fit comfortably? Your future self will thank you for considering these details.

Effective car buying is about balancing practicality with financial wisdom. Are you ready to make a confident decision?

For more insights on loan calculators and affordability tips, visit Consumer Reports Car Buying Guide.

Frequently Asked Questions

How Much Car Can I Afford 20 4 10 Rule?

The 20/4/10 rule suggests a 20% down payment, a 4-year loan term, and car payments under 10% of monthly income. Ensure total vehicle expenses, including insurance and maintenance, stay below 10% of monthly income. This helps maintain financial health and prevents overspending on a car purchase.

What Not To Say When Financing A Car?

Avoid mentioning your maximum budget or desperation for the car. Don’t reveal your monthly payment limit. Never say you’re just browsing or uncertain about financing. Avoid disclosing your credit score details. Stay clear of discussing other dealer offers.

What Is The 20 3 8 Rule When Buying A Car?

The 20/3/8 rule suggests a 20% down payment, a three-year loan term, and car expenses below 8% of monthly income.

How Much Is A $30,000 Car Payment for 60 Months?

A $30,000 car payment over 60 months depends on interest rates. At 5% interest, the monthly payment would be approximately $566. Use an online loan calculator for precise figures tailored to your interest rate. Always consult with your financial institution for exact numbers.

Conclusion

The 20/4-10 Rule guides smart car buying. Spend 20% upfront. Finance for four years only. Keep car expenses under 10% of monthly income. This rule helps manage finances. Avoids overspending. Encourages responsible budgeting. You enjoy peace of mind. Reduces financial stress.

Makes car ownership more affordable. Stick to the rule. Enjoy your new car wisely.

If you’re also planning long-term car care, check out our Car Detailing Products guide for budget-friendly maintenance. Happy driving!